India’s GDP Refresh

A Guide to the 2022-23 Rebasing

Why Rebase Now? (The Motivation)

India’s GDP is currently benchmarked to 2011-12—a “mirror” that is now over a decade old. Since then, the rollout of GST, the explosion of digital payments (UPI), and the structural shift post-pandemic have fundamentally transformed the economy.

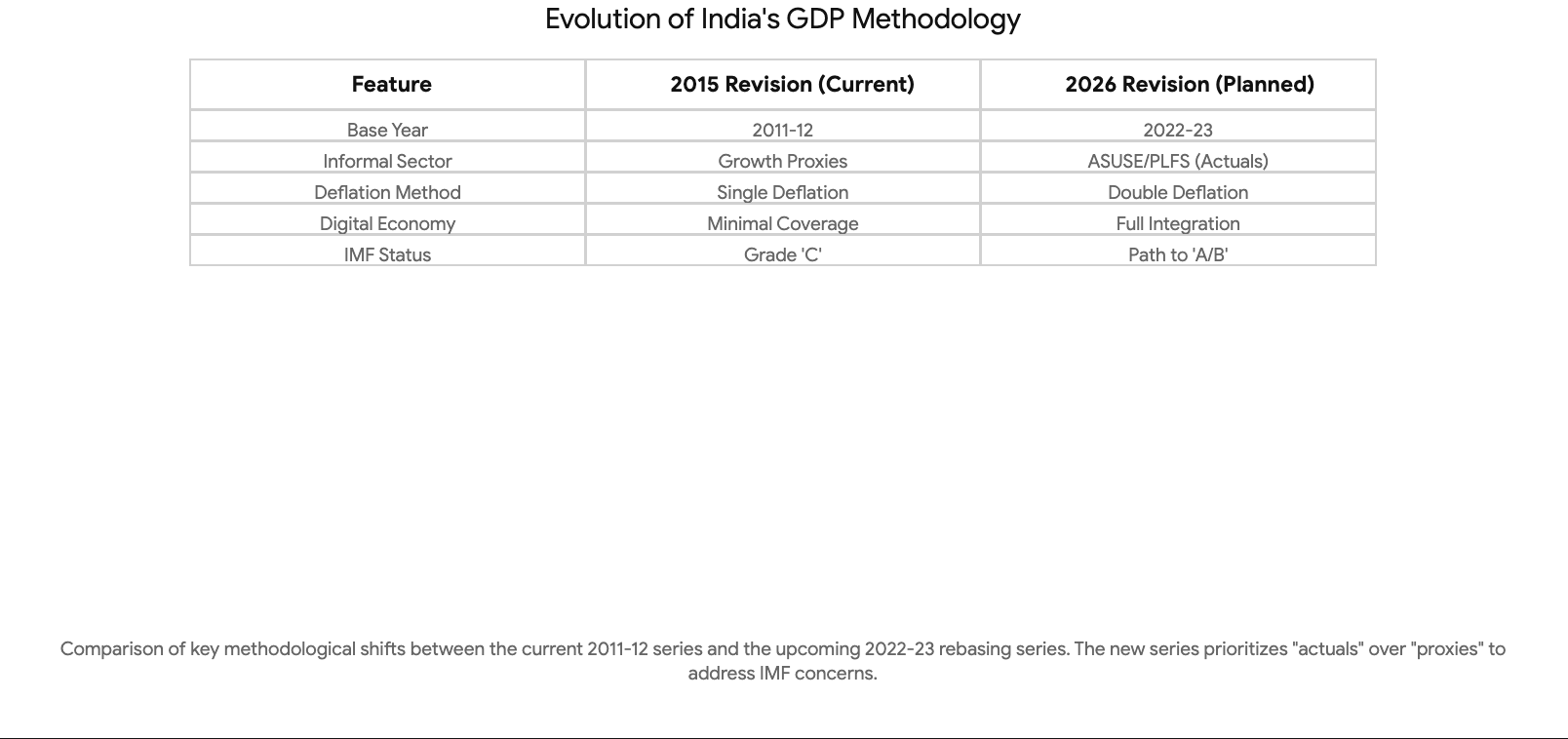

The International Monetary Fund (IMF) recently assigned India a “C” grade for national accounts, citing the outdated base year as a primary shortcoming for effective surveillance. Rebasing to 2022-23 aims to fix this “credibility gap” by capturing the modern, formalized India.

The motivation for rebasing is anchored in three primary objectives.

First, it is essential to capture up-to-date price relatives, ensuring that volume estimates of economic activity are not distorted by outdated cost structures.

Second, it allows for a widening of sectoral coverage by incorporating new databases that have matured since the last revision, such as the MCA-21 database and granular GST filings.

Third, it aligns India with the evolving international standards, specifically transitioning from the SNA 2008 framework toward the emerging requirements of SNA 2025. Without this recalibration, the headline growth figures risk becoming unrepresentative of the "new India," potentially leading to sub-optimal policy decisions and misinformed investment strategies.

Comparing the Shifts: 2015 vs. 2026

The 2015 revision (shifting from 2004-05) was controversial, with some experts claiming it overestimated growth by up to 2.5 percentage points. The 2026 update addresses this through technical fixes like Double Deflation, ensuring that falling raw material costs aren't optically misread as production growth.

The choice of 2022-23 as the new base year is strategically grounded in the need for a "normal" reference point. The fiscal years 2019-20 and 2020-21 were marred by the global health crisis, which suppressed industrial output, disrupted supply chains, and temporarily altered household expenditure baskets in ways that were not representative of long-term trends. By 2022-23, high-frequency indicators (HFIs) suggested a stabilization of economic activity, characterized by a resurgence in domestic demand and a normalization of the services sector. This stabilization is crucial because the weights assigned to various industries in the base year determine the perceived contribution of those industries to the overall economy for years to come.

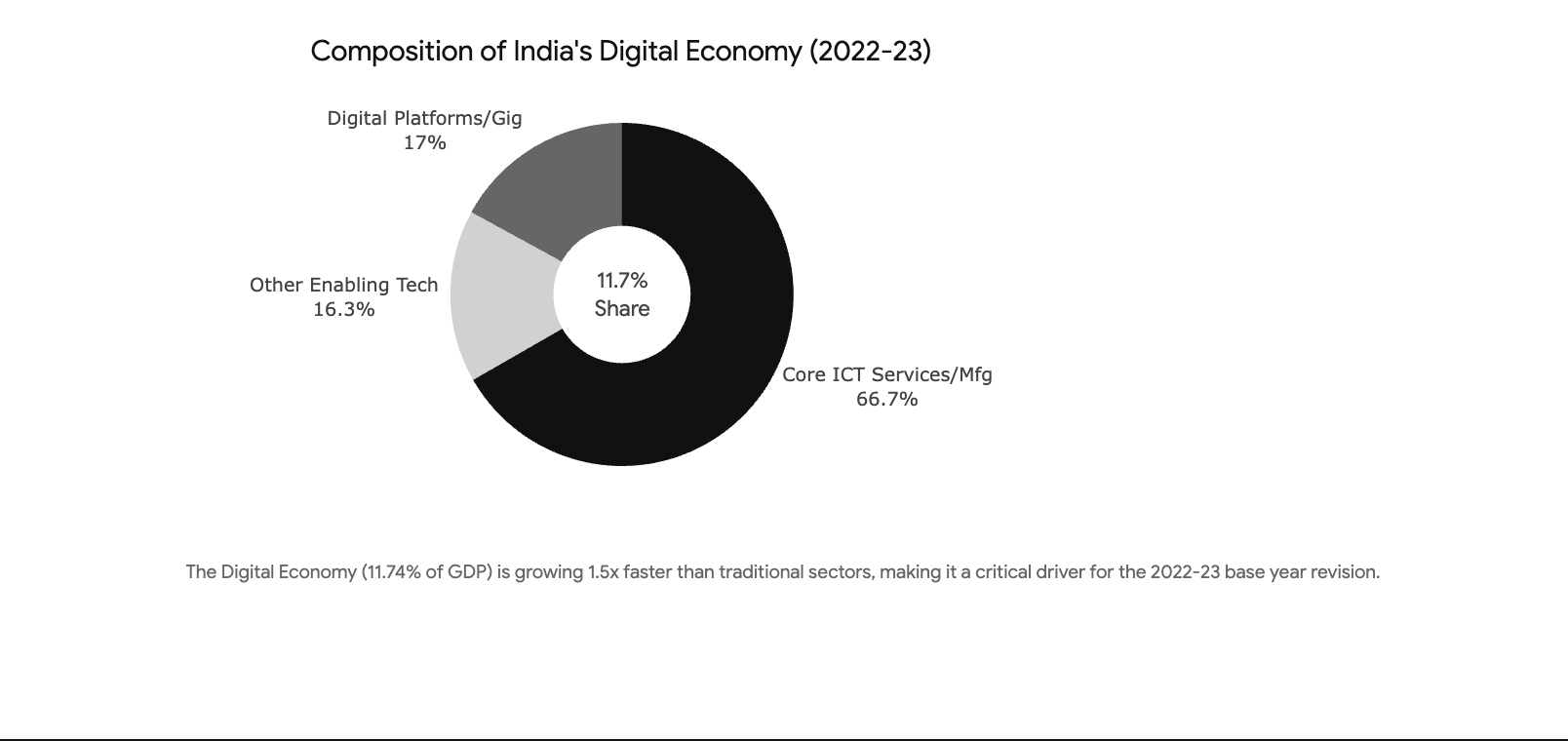

The New Drivers: Digital & Gig Economy

Digitalization is the hero of this series. The digital economy now contributes 11.74% of GDP and is growing nearly 1.5x faster than traditional sectors. For the first time, the series will use "actuals" from 14.6 million gig workers and UPI transaction logs rather than historical proxies.

The Digital Economy: A Structural Powerhouse

The digital economy has undergone a metamorphosis over the last decade. In 2022-23, it was estimated to contribute 11.74% of India’s GDP, equivalent to approximately $402 billion (₹31.64 lakh crore). This sector is not only growing rapidly—at an annual rate of 17.3% compared to the overall economy’s 11.8%—but it is also nearly five times more productive than the rest of the economy.

The new series will focus on three key pillars of the digital economy:

Digital Intermediaries and Platforms: This sub-sector, including e-commerce, app-based aggregators, and fintech, contributed roughly 2% of GVA in 2022-23 and is projected to grow by 30% annually.

ICT Manufacturing: The production of electronic components and communication equipment, bolstered by the Production Linked Incentive (PLI) schemes, is a core component that the 2011-12 series fails to capture with sufficient granularity.

The Gig Economy: Digital platforms have created a workforce of 14.67 million workers (2.55% of the total workforce). The 2022-23 rebasing will utilize data from e-way bills, FASTag, and UPI transactions to track the output of these workers, providing a clearer picture of consumption and service delivery.

Renewable Energy and Green Growth

The 2011-12 base was established at a time when coal was the nearly exclusive driver of India’s energy sector. Since then, renewable energy capacity has expanded exponentially. The new series will provide a dedicated framework for calculating the GVA of solar, wind, and green hydrogen. Moreover, as India aligns with the sustainability goals of SNA 2025, the new series may begin to incorporate “Green Accounts,” which treat the depletion of natural resources as a cost of production rather than just a volume change in assets.

Modernized Logistics and Services

The logistics sector has transitioned from fragmented, transport-only operations to technology-integrated networks. The 2022-23 series will leverage the digitalization of the logistics chain to better estimate the “Trade, Hotels, Transport, and Communication” sector, which has shown resilient double-digit growth (12.3%) in recent final estimates. The inclusion of air cargo and intra-city delivery networks will ensure that the services-driven nature of modern Indian commerce is fully reflected in the GVA.

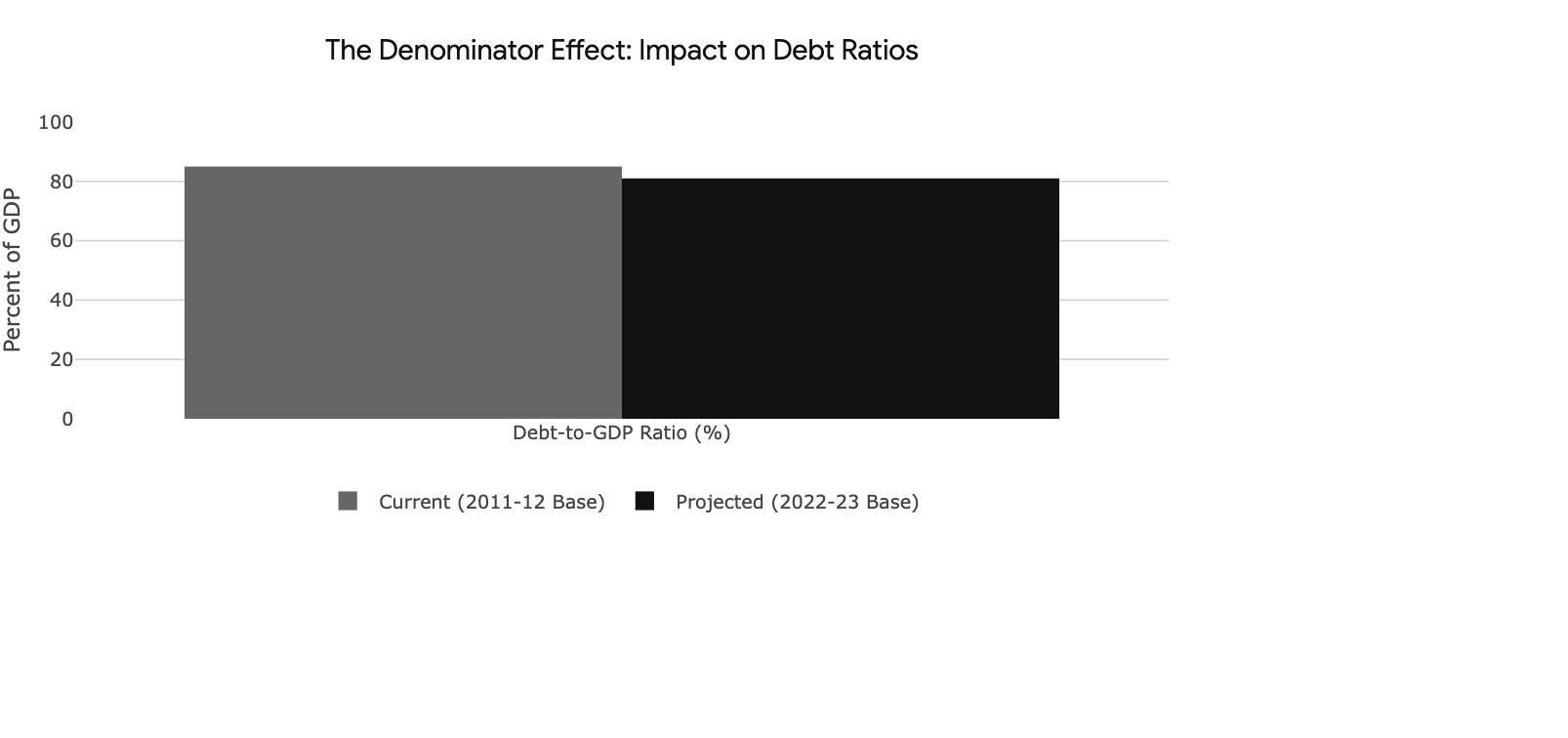

The “Denominator Effect” (Impact on Numbers)

Rebasing typically increases the absolute size of nominal GDP. Current estimates suggest a jump from ~₹297 lakh crore to ~₹325 lakh crore.

Lower Debt Ratios: A larger GDP base makes India’s debt (currently ~85% of GDP) appear smaller (~81%) on paper.

Fiscal Space: Higher nominal numbers help the government meet deficit targets more easily, bolstering sovereign creditworthiness.

One of the most anticipated and sensitive aspects of the rebasing is the release of the "back-series" data, scheduled for February 2026. This data will recalculate the growth rates for the years since 2011-12 using the new methodology. If the new series shows higher growth for the post-2020 period, it would validate the narrative of a "V-shaped recovery" and structural resilience. Conversely, any significant deviation could trigger a renewed debate about data credibility. Economists will closely watch how the historical series aligns with newer methods and data sources such as GST filings and corporate balance sheets.

The Investor Verdict

Better data translates to lower perceived risk. S&P has already upgraded India’s outlook to “positive,” citing the sustainable growth and fiscal discipline these statistics will now more accurately reflect. A successful shift could trigger a formal rating upgrade and multi-billion dollar inflows as India moves toward an “A” grade in global data adequacy.

The transparency and accuracy of GDP data influence India's weight in global indices like the MSCI Emerging Markets Index. As of July 2025, India’s weight in this index reached a record 18.2%, more than double its weight from five years ago. A robust and rebased GDP series increases the "investability" of the Indian market, as passive fund managers and global institutional investors require high-quality, comparable data.

India’s recent inclusion in the J.P. Morgan Emerging Market Global Diversified Index—with a projected 10% weight—is expected to generate over $23 billion in inflows into government bonds by early 2025. The success of this inclusion is predicated on macroeconomic stability and data transparency. A "C" grade from the IMF can act as a drag on these inflows, as some mandates require "B" or higher for core allocations.

Conclusion

The rebasing of India’s GDP from 2011-12 to 2022-23 is more than a technical update; it is a foundational step in the nation’s journey toward becoming a developed economy (”Viksit Bharat”) by 2047. By modernizing the base year, adopting double deflation, and leveraging real-time digital databases, India is addressing the long-standing critiques of its statistical architecture and providing a more transparent, accurate roadmap for policymakers and investors alike.

The 2022-23 rebasing is a strategic necessity to ensure the permanence of these capital flows by aligning India’s statistical "A-grade" timeliness with "A-grade" data quality.